Executive Sumary:

A 12-year-old life insurance policy originally designed for tax-free growth and generational wealth transfer had gone largely dormant. High internal costs, expensive and outdated riders, and a complete absence of active management had left it stagnating, with cash value not only failing to grow but actively declining. RM Legacy Group performed a comprehensive structural audit, eliminated unnecessary riders, repositioned allocations into institutional-grade options, and fully redesigned the policy for long-term efficiency.

The result was transformative. The same policy, without a single dollar of new premium, was redesigned to project $2.8 million in future tax-free retirement income, more than double what the original structure would have delivered. The death benefit for heirs remained fully intact throughout the process.

This Legacy Rescue engagement illustrates one of the most important and underappreciated realities in advanced insurance planning: the policies most in need of attention are often the ones that have never been reviewed.

When Autopilot Becomes Expensive:

When a long-standing client brought us a twelve-year-old life insurance policy for review, the story it told was immediately familiar. The policy had been designed in the early 2010s as a cornerstone of a tax-free growth and legacy transfer strategy, thoughtfully structured at inception and then quietly forgotten. Over the decade that followed, the financial landscape shifted, carrier product offerings evolved, and new institutional allocation options emerged. The policy did not evolve with them.

What our team found was a structure that had once been purposeful but had drifted into inefficiency through inaction. Expensive riders that had made sense at inception now served no meaningful function. Asset allocations were heavily concentrated in fixed crediting accounts generating less than three percent annually. Internal charges continued accumulating year after year, quietly eroding the very cash value the policy was designed to grow.

The client had been paying premiums faithfully for over a decade. Yet their cash value was declining. Annual statements were difficult to interpret. Projections were unclear. The intended balance between protection and accumulation had been lost entirely, not through any single decision, but through the slow, compounding cost of neglect.

eroded both growth potential and clarity of purpose.

The client had been paying premiums faithfully, yet their cash value was actually declining. The annual statements were difficult to interpret, the projections unclear, and the intended balance between protection and growth had been lost. Like many legacy policies, the structure had simply been left on autopilot, assuming that “set and forget” would be sufficient. Unfortunately, in an evolving market with changing carrier products and new institutional allocation options, inaction proved costly.

Diagnosing the Problem:

Our first step was a complete forensic audit of the policy, examining every structural element in detail: internal rate assumptions, expense loads, rider costs, crediting methodology, and investment allocations. The findings were unambiguous.

Nearly 25% of annual charges were being consumed by outdated riders that had long outlived their usefulness. The asset allocation was heavily weighted toward fixed crediting strategies generating below-market returns. The compounding effect of these two factors over twelve years had not only suppressed growth but had begun to actively erode cash value in the later policy years.

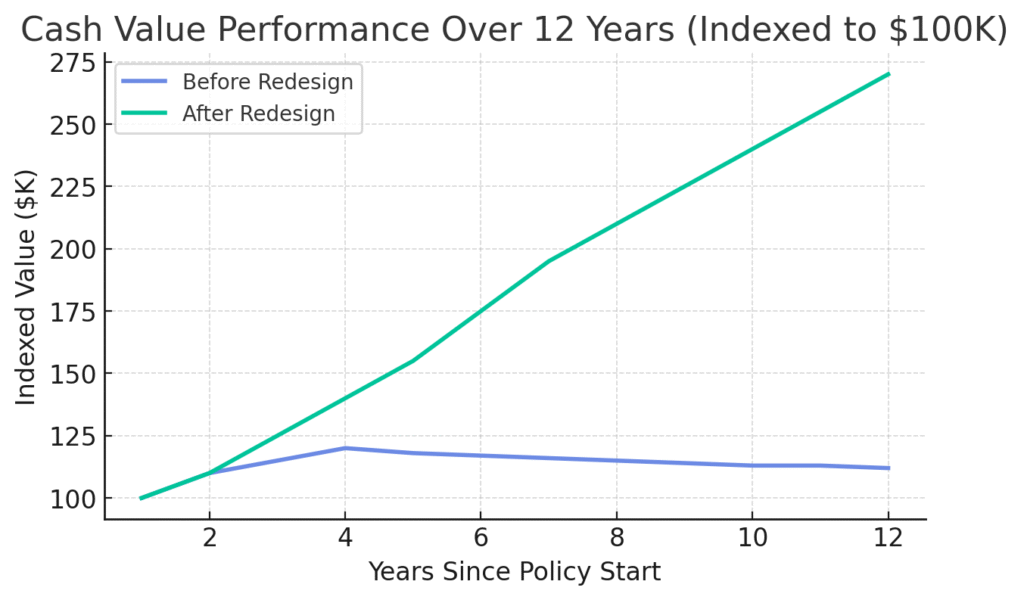

The chart above tells the story with clarity. The blue line shows how cash value grew modestly in the early years before flattening and then beginning a gradual decline as internal costs outpaced the returns generated by the fixed allocation. The green line represents the redesigned trajectory, one that regains momentum immediately following the intervention and compounds meaningfully upward over the remaining policy horizon.

The data deliver a simple but important truth: even the most conservatively structured plan requires periodic review and engineering. Without it, inefficiency is not a possibility. It is a certainty.

The Redesign:

Our objective was never to replace the policy. It was to rescue it, restructure it, and restore its purpose. We began by identifying and eliminating every rider that no longer served a meaningful function within the client’s current financial picture, immediately reducing the internal cost burden and freeing capital to compound inside the policy rather than fund unnecessary provisions.

The asset allocation was completely repositioned. Fixed crediting strategies that had been generating sub-market returns were trimmed significantly, and the freed allocation was redirected into institutional-grade indexed strategies with substantially stronger long-term growth potential. The crediting methodology was re-sequenced to align with current market participation caps, ensuring the policy was capturing available upside efficiently across each crediting period.

The Results:

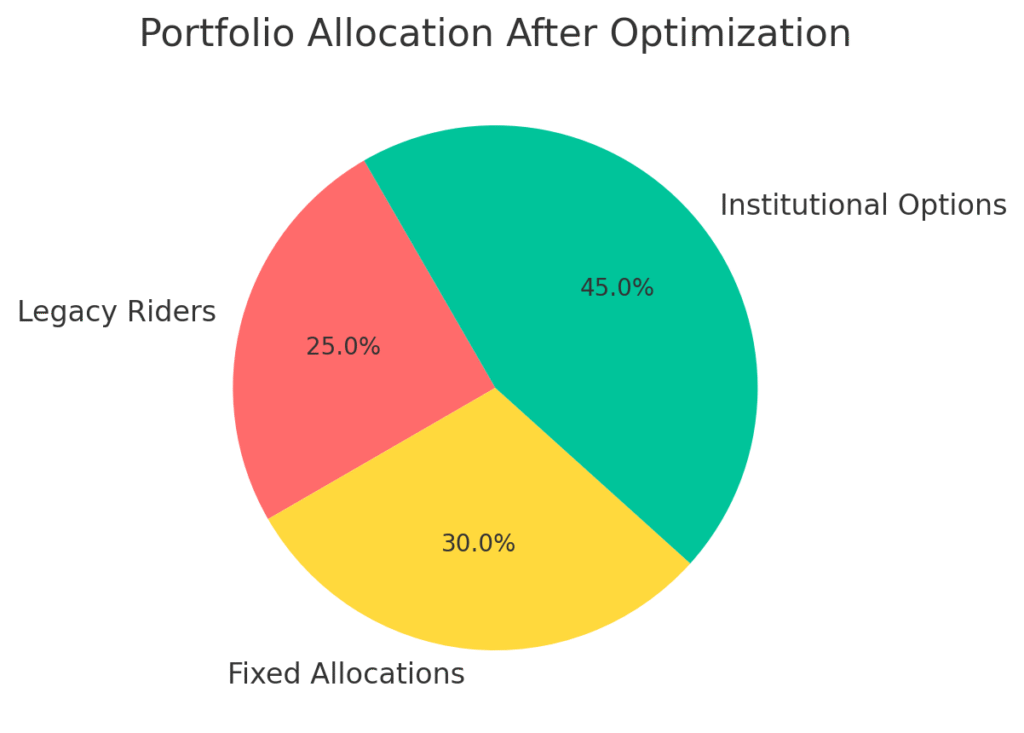

As the allocation chart illustrates, the optimized structure shifted the policy from one dominated by fixed and rider costs to one where 45% of the structure is now deployed in institutional options designed for long-term accumulation, with fixed allocations reduced to 30% and legacy rider costs compressed from 25% to effectively zero.

A disciplined policy-loan strategy was layered into the redesign to enable tax-free income distribution in retirement without disrupting the underlying cash value compounding. Every modification was stress-tested against IRS Section §7702 requirements and Modified Endowment Contract guidelines to ensure the redesigned structure maintained full compliance and long-term structural integrity.

No new premiums were required. The entire transformation was achieved through intelligent restructuring of assets that were already inside the policy.

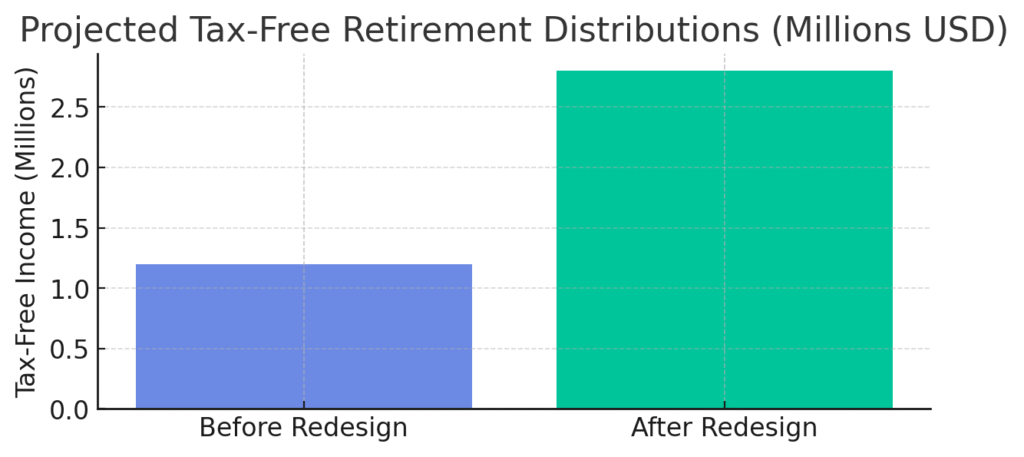

The redesigned structure now projects $2.8 million in future tax-free retirement distributions, up from approximately $1.2 million under the original structure. That is a $1.6 million improvement in projected lifetime income achieved without a single dollar of additional premium, without introducing external leverage, and without compromising the death benefit available to the client’s heirs.

Beyond the income improvement, the structural overhaul created meaningful new optionality for the client. The policy now offers the flexibility to draw tax-free income in retirement, preserve and grow the legacy benefit for heirs, or rebalance allocations as market conditions and personal objectives evolve over time. What had been a dormant asset with fading relevance became an active, tax-efficient instrument capable of serving both retirement income and estate planning objectives simultaneously.

The improved internal efficiency did not simply revive the growth trajectory. It restored the policy to its original purpose, and then some.

What This Case Study Means for Policyholders:

If you own a life insurance policy that is more than five years old and has never been independently reviewed, the probability that it is operating below its potential is significant. Carrier products evolve. Crediting options improve. Internal cost structures can be optimized. Riders that once made sense may now be consuming value without delivering meaningful benefit.

Most policyholders never discover this because no one ever tells them. The original selling agent has moved on. The carrier has no incentive to proactively recommend a restructuring. And the annual statement, dense with figures and projections, offers little clarity about whether the policy is performing as it should.

At RM Legacy Group, in-force policy review and optimization is one of our core capabilities. We have recovered millions of dollars in projected lifetime value for clients simply by taking the time to look carefully at what others had left on autopilot.

Precision. Purpose. Performance.

The $1.6 million improvement in projected tax-free income documented in this case study was not the result of better market conditions, higher contribution levels, or increased risk tolerance. It was the result of one thing: someone finally taking the time to look.

If you have a life insurance policy that has not been reviewed in the past three to five years, we welcome the opportunity to conduct a complimentary in-force audit and show you exactly where your policy stands, and what it could be doing instead.