Executive Summary

Transforming Standard Solutions into Exceptional Outcomes

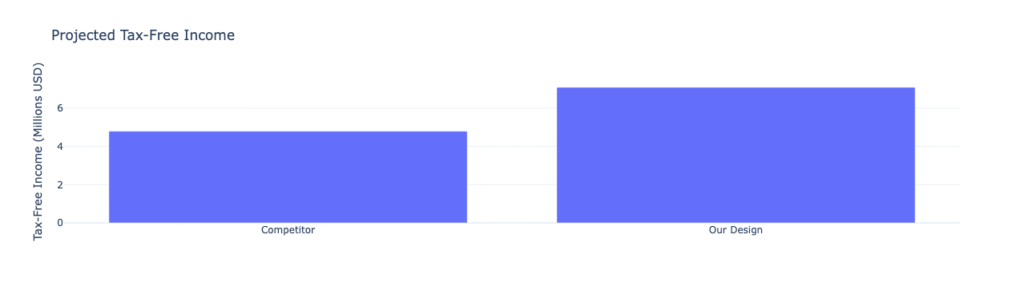

A successful entrepreneur approached RM Legacy Group with a straightforward but consequential objective: contribute $250,000 annually into a life insurance policy designed to deliver maximum tax-free retirement income while securing meaningful long-term legacy protection for his family. A competing firm had already proposed a solution, presenting an illustration that projected $4.8 million in future tax-free income. Respectable on its face. Far from optimized in practice.

Through a meticulous structural redesign, RM Legacy Group restructured the premium allocation, reduced internal policy costs, and sequenced contributions within precise IRS compliance frameworks. The result was striking. The very same $250,000 annual contribution now projected $7.1 million in tax-free retirement income, an improvement of $2.3 million, or nearly 50% more value, achieved without adding a single dollar of additional contribution, risk, or leverage.

This case study is a direct illustration of one of RM Legacy Group’s core convictions: structure outperforms speculation. The hidden value in most life insurance strategies is not found by taking more risk. It is found by eliminating the inefficiency that standard designs routinely leave on the table.

The Challenge of “Standard” Designs

The competing firm’s illustration relied on an off-the-shelf policy structure typical of what most insurance distributors present to clients. These template designs tend to load disproportionately higher internal costs into the early accumulation years, fail to fully optimize the balance between base insurance coverage and supplemental riders, and make no meaningful attempt to compress the policy’s internal cost structure in favor of long-term cash value growth.

The practical consequence of these design choices is lower net cash value accumulation year after year, diminished tax-free loan capacity in retirement, and a long-term income projection that significantly understates what the same premium dollars could actually produce inside a properly engineered structure.

In short, the client was unknowingly paying for inefficiencies that had been quietly baked into a one-size-fits-all template. No one had taken the time to actually engineer the policy around his specific objectives.

The Redesign: Engineering Without Extra Risk

RM Legacy Group’s approach was disciplined and deliberately structural. Rather than seeking higher projected returns through more aggressive index selections or speculative assumptions, every optimization lever applied was rooted in design efficiency, cost compression, and compliance precision.

Premium was reallocated between the base policy and rider components to maximize the ratio of cash value accumulation to insurance cost. Internal charges were compressed to the lowest viable level consistent with the desired death benefit and income objectives. The premium funding sequence was carefully phased to maximize compounding efficiency across the full accumulation horizon while adhering strictly to IRC §7702 compliance tests, including both the Cash Value Accumulation Test and the Guideline Premium Test.

Critically, the design was engineered to avoid Modified Endowment Contract classification by sequencing contributions with precision, preserving the policy’s full tax-advantaged loan and withdrawal treatment throughout the client’s lifetime.

Rather than chasing performance, RM Legacy Group created a legal and structural framework that preserved the safety and guarantees of the insurance contract while unlocking significantly higher tax-free income capacity. The additional $2.3 million was not generated by taking more risk. It was recovered from the drag that the standard design had quietly surrendered.

Side-by-Side Results

The numbers speak for themselves. The competing firm’s template illustration projected $4.8 million in available tax-free retirement income. The RM Legacy Group optimized structure, funded with the identical $250,000 annual contribution, projected $7.1 million in tax-free income, an uplift of $2.3 million achieved entirely through structural improvement with no additional risk, no additional leverage, and no change in the client’s annual commitment.

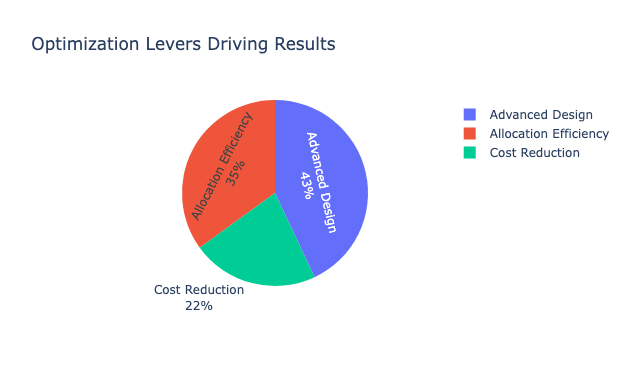

As illustrated in the optimization breakdown above, the improvement was driven by three distinct levers working in combination: advanced policy design, allocation efficiency, and internal cost reduction. Each lever contributed meaningfully to the outcome. Together, they produced a result that most clients would never discover working with a standard distributor.

Compliance as the Backbone

The durability and long-term integrity of this outcome rests entirely on a compliance-first design philosophy. Every structural decision made during the redesign process was tested against the applicable legal and regulatory framework before implementation.

The policy design was validated against both the Section §7702 Cash Value Accumulation Test and the Guideline Premium Test to ensure full compliance with life insurance tax treatment requirements. Ownership structure was carefully reviewed and coordinated to avoid Goodman Triangle taxation issues, which can arise when three separate parties hold the roles of owner, insured, and beneficiary. Trust planning was integrated to ensure that policy proceeds could flow efficiently through an Irrevocable Life Insurance Trust or dynasty trust structure in alignment with the client’s estate planning objectives.

Loan mechanics were specifically modeled using participating loan provisions, ensuring that the policy’s underlying cash value continued to compound at the full crediting rate even during periods when income was being actively distributed. This single design choice, often overlooked in standard illustrations, meaningfully increases the long-term sustainability of the income strategy.

The result is a policy that is not only structurally powerful but legally sound, fully compliant, and built to perform reliably across decades without requiring structural modification.

What This Means for Sophisticated Families

For high-net-worth individuals and families considering life insurance as a component of their broader wealth strategy, the lesson this case study offers is both clear and actionable. The difference between a good outcome and an exceptional one is rarely found in the product itself. It is found in how the product is designed, engineered, and integrated into the client’s full financial picture.

The additional $2.3 million in projected tax-free income recovered in this engagement represents value that the standard illustration had quietly surrendered to internal inefficiency. It required no additional contribution, no additional risk, and no compromise of the client’s legacy objectives. It required only the willingness to take the time to engineer the structure properly from the beginning.

Beyond the income optimization, the redesigned structure offered enhanced liquidity through policy loan access, reducing the client’s dependence on the sale of operating business interests or illiquid assets to fund retirement income needs. And with trust ownership carefully coordinated and beneficiaries precisely aligned, the plan advanced the family’s multigenerational estate planning objectives in a way that the original proposal never could have.

Precision. Purpose. Performance.

At RM Legacy Group, we believe that every client who has been shown a standard illustration deserves to know what a properly engineered alternative would look like. The gap between what most designs project and what an optimized structure can actually deliver is, in many cases, measured in millions of dollars of tax-free value that simply never needed to be left behind.

If you have an existing policy illustration or a current life insurance program that has never been independently reviewed for design efficiency, we welcome the opportunity to conduct a complimentary analysis and show you what your premium dollars could actually be doing.